Pix has been revolutionizing Brazil’s payments landscape since its launch by the Brazilian Central Bank in 2020. Designed as an instant, account-to-account (A2A) transfer system, Pix is continually reducing dependence on traditional payment methods such as cash, Boletos, and debit cards.

Pix is transforming the payment system by increasing efficiency, lowering costs, promoting inclusion, and driving competition. The Central Bank continues to expand Pix’s use cases, boosting its relevance across segments:

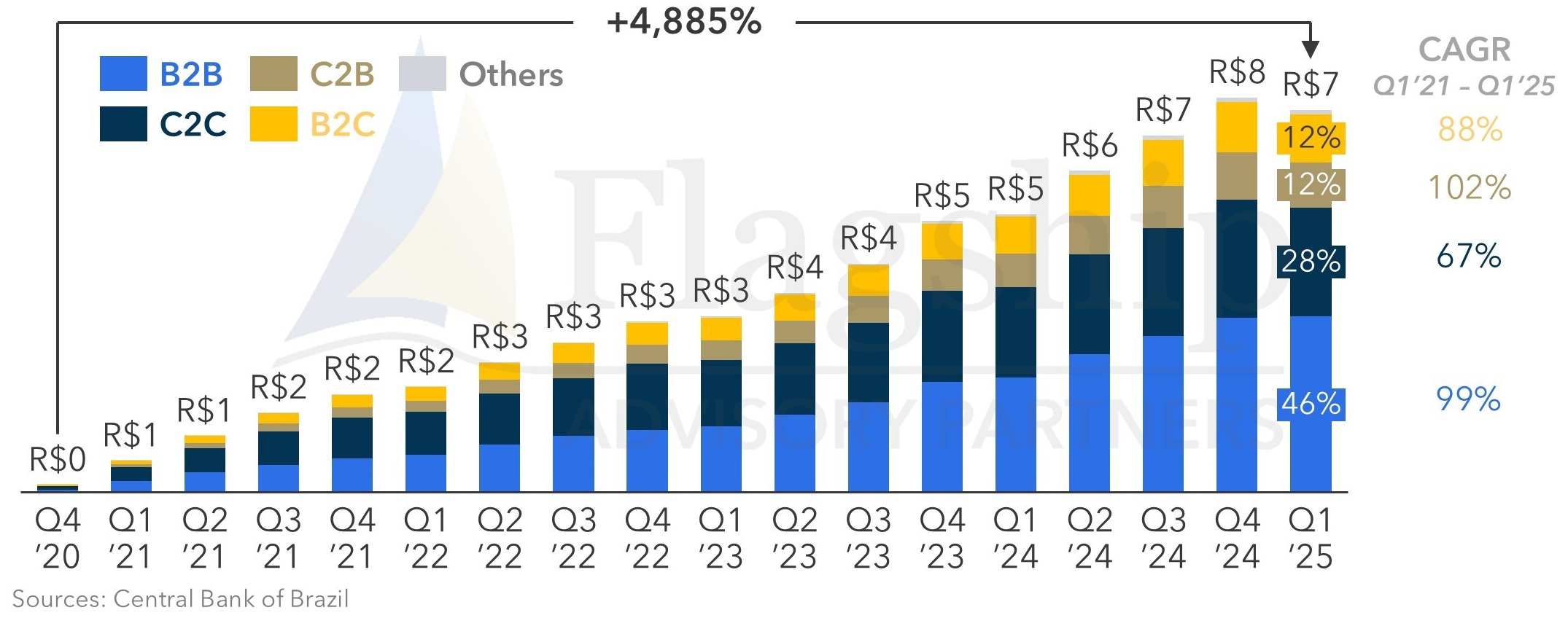

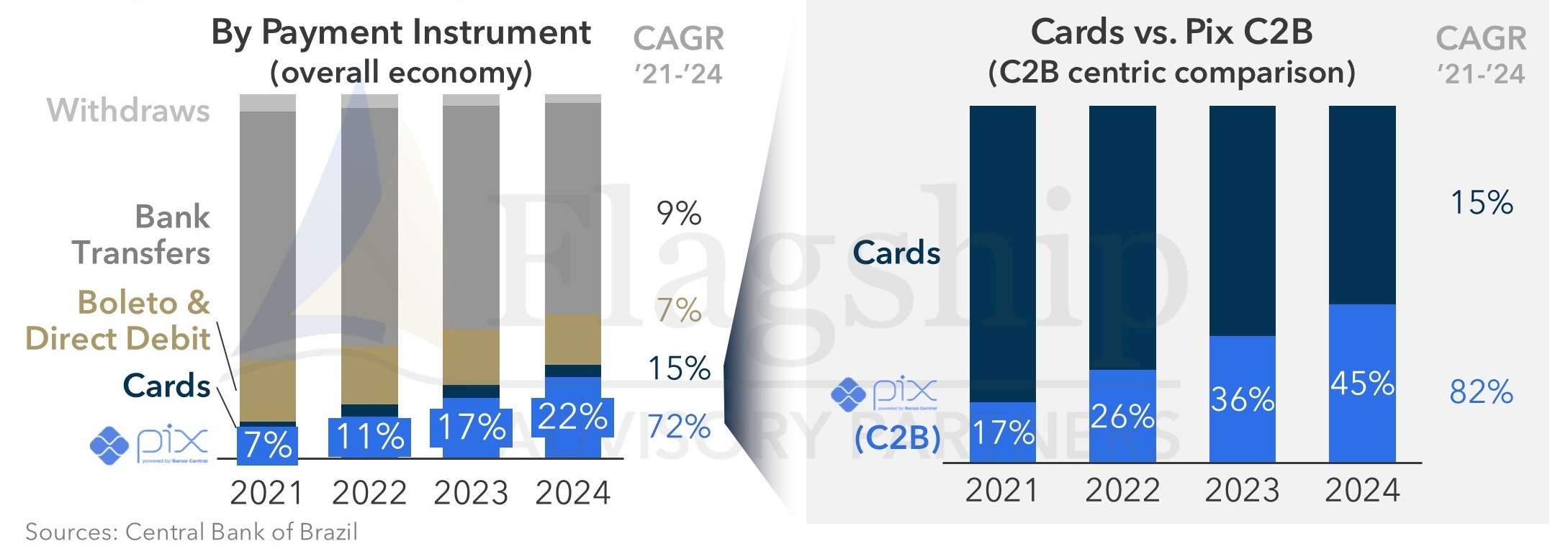

Pix is primarily replacing cash, Boleto, and bank transfers, while also gaining ground against cards—mainly debit, given Pix’s A2A nature. PSPs have reported strong Pix-driven payment volume growth, especially from the displacement of cash, but this has pressured margins as Pix has lower fees than cards. While this displacement of cash is net positive, as Pix starts cannibalizing card volumes, the impact turns more negative.

Pix is primarily replacing cash, Boleto, and bank transfers, while also gaining ground against cards—mainly debit, given Pix’s A2A nature. PSPs have reported strong Pix-driven payment volume growth, especially from the displacement of cash, but this has pressured margins as Pix has lower fees than cards. While this displacement of cash is net positive, as Pix starts cannibalizing card volumes, the impact turns more negative.

Pix monetization focuses on business acceptance fees, generally lower than cards but varying by merchant size and banking relationship. Micro / small merchants pay sticker pricing below debit cards, while larger merchants can negotiate even smaller fees when bundled with other banking services.

Cards, especially in credit and installments, remain highly profitable and are growing at 15% per year, but face increasing pressure as Pix expands. The launch of Pix Credit may add further tension, as the same banks providing credit for Pix transactions also benefit from interchange revenues as card issuers.

Please do not hesitate to contact Pedro Giesta at Pedro@FlagshipAP.com with comments and questions.